Unlocking Your Financial Future: 5 Essential Retirement Accounts Explained

Introduction

With great pleasure, we will explore the intriguing topic related to Unlocking Your Financial Future: 5 Essential Retirement Accounts Explained. Let’s weave interesting information and offer fresh perspectives to the readers.

Unlocking Your Financial Future: 5 Essential Retirement Accounts Explained

Retirement. It’s a word that often evokes a mix of excitement and anxiety. Excitement for the freedom and leisure it promises, and anxiety about the financial security it requires. Navigating the world of retirement accounts can feel overwhelming, especially for those just starting their financial journey. But fear not! This comprehensive guide will demystify the 5 essential retirement accounts, empowering you to make informed decisions and secure a comfortable future.

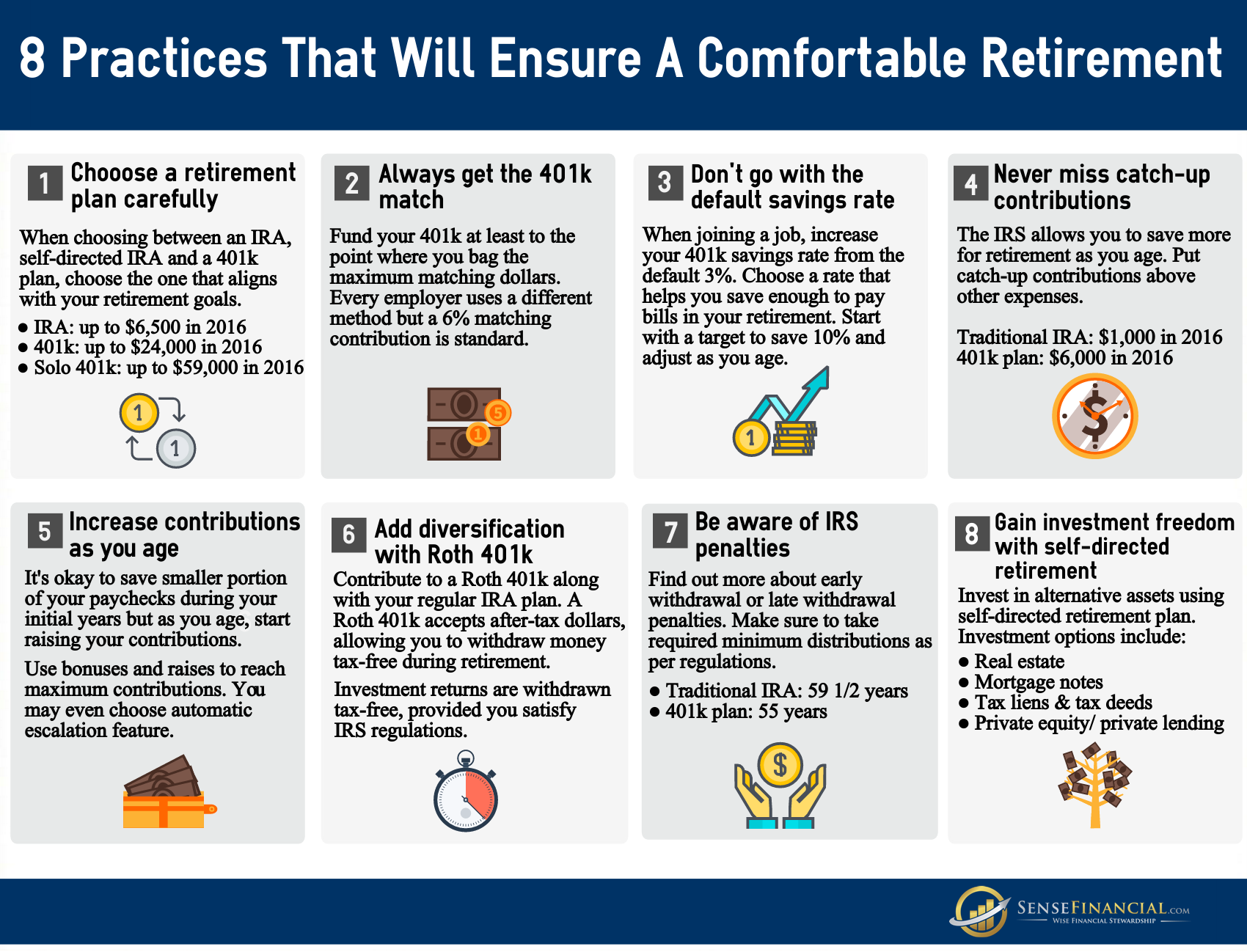

1. The Traditional IRA: A Time-Tested Classic

The Traditional Individual Retirement Account (IRA) is a cornerstone of retirement planning. This account allows you to contribute pre-tax dollars, reducing your current tax liability. The money grows tax-deferred, meaning you won’t pay taxes until you withdraw it in retirement.

Here’s what makes the Traditional IRA attractive:

- Tax Advantages: The pre-tax contributions and tax-deferred growth can significantly reduce your overall tax burden.

- Flexibility: You can choose from a wide range of investment options, including stocks, bonds, mutual funds, and ETFs.

- Accessibility: Anyone with earned income can contribute to a Traditional IRA, regardless of their employer’s participation in a retirement plan.

However, there are some drawbacks to consider:

- Required Minimum Distributions (RMDs): You must begin withdrawing money from your Traditional IRA after age 72, and these distributions are taxed as ordinary income.

- Taxable Withdrawals in Retirement: While you enjoyed tax savings during your working years, withdrawals in retirement are taxed at your ordinary income tax rate.

- Income Limits: If your income exceeds a certain threshold, you may not be able to contribute the full amount or may be ineligible to contribute at all.

2. The Roth IRA: A Tax-Free Future

The Roth IRA offers a unique twist on retirement savings. Instead of deducting contributions from your current income, you contribute after-tax dollars. This means you pay taxes upfront, but your withdrawals in retirement are completely tax-free.

The Roth IRA’s strengths lie in its tax-free nature:

- Tax-Free Withdrawals: Enjoy the fruits of your labor without paying any taxes on withdrawals in retirement.

- No RMDs: You’re not required to take distributions from your Roth IRA, allowing your savings to continue growing tax-free.

- Potential for Tax Savings: If you expect to be in a higher tax bracket in retirement than you are now, the Roth IRA can be a valuable tool for minimizing your tax liability.

However, there are some downsides to consider:

- No Current Tax Deduction: You don’t get an immediate tax break on your contributions, unlike the Traditional IRA.

- Income Limits: Similar to the Traditional IRA, there are income limits for contributing to a Roth IRA.

- Younger Savers Benefit Most: The longer your money grows tax-free in a Roth IRA, the greater the potential for tax savings in retirement.

3. 401(k): Employer-Sponsored Savings

If you work for a company that offers a 401(k) plan, you have access to a powerful retirement savings tool. A 401(k) allows you to contribute pre-tax dollars from your paycheck, which are then invested in a variety of options.

The 401(k) offers several compelling benefits:

- Employer Matching: Many employers offer matching contributions, essentially giving you free money for your retirement savings.

- Tax Advantages: Your contributions are tax-deductible, and your investments grow tax-deferred.

- Convenience: Contributions are automatically deducted from your paycheck, making it easier to save consistently.

However, there are some points to be mindful of:

- Limited Investment Options: The investment options available within a 401(k) may be more limited than those offered by a Traditional or Roth IRA.

- Early Withdrawal Penalties: Withdrawing money from your 401(k) before age 59 1/2 typically incurs penalties, unless you qualify for an exception.

- Vesting Schedule: Some employers have a vesting schedule, which means you may not own the full amount of your employer’s matching contributions until you’ve worked for the company for a certain period.

4. 403(b): Retirement Savings for Non-Profits

If you work for a non-profit organization, a 403(b) plan is your equivalent to a 401(k). It operates similarly, allowing you to contribute pre-tax dollars to a tax-deferred retirement account.

The 403(b) offers many of the same benefits as the 401(k):

- Tax Advantages: Pre-tax contributions and tax-deferred growth provide significant tax savings.

- Employer Matching: Some non-profit employers offer matching contributions, boosting your retirement savings.

- Convenience: Automatic contributions from your paycheck make saving a breeze.

However, the 403(b) also shares some drawbacks with the 401(k):

- Limited Investment Options: The range of investment options may be more restricted compared to IRAs.

- Early Withdrawal Penalties: Withdrawing money before age 59 1/2 typically incurs penalties.

- Vesting Schedule: Similar to 401(k) plans, there may be a vesting schedule for employer matching contributions.

5. The Solo 401(k): Self-Employment Savings

If you’re self-employed or own a small business, a Solo 401(k) offers a unique opportunity to save for retirement. It combines the benefits of a 401(k) with the flexibility of an IRA.

The Solo 401(k) stands out for its flexibility and tax advantages:

- Combined Employer and Employee Contributions: You can contribute both as an employee and an employer, maximizing your savings potential.

- Tax Advantages: Your contributions are tax-deductible, and your investments grow tax-deferred.

- Higher Contribution Limits: You can contribute significantly more than you could with a traditional IRA.

However, there are some aspects to consider:

- Administrative Complexity: Managing a Solo 401(k) requires more administrative effort than a traditional IRA.

- Investment Options: You’ll need to choose your own investment options, which may require additional research and effort.

- Early Withdrawal Penalties: Withdrawing money before age 59 1/2 typically incurs penalties.

Choosing the Right Retirement Account for You

The best retirement account for you depends on your individual circumstances, financial goals, and risk tolerance. Here’s a quick guide to help you decide:

- Traditional IRA: Ideal for those seeking immediate tax savings and expecting to be in a lower tax bracket in retirement.

- Roth IRA: Suitable for those who prefer tax-free withdrawals in retirement and expect to be in a higher tax bracket.

- 401(k): A valuable option if your employer offers a matching contribution, providing a significant boost to your savings.

- 403(b): A good choice for employees of non-profit organizations, offering similar tax benefits to the 401(k).

- Solo 401(k): An excellent option for self-employed individuals and small business owners seeking flexibility and higher contribution limits.

Beyond the Basics: Maximizing Your Retirement Savings

Understanding the different retirement accounts is just the first step. To truly unlock your financial future, you need to implement strategies for maximizing your savings potential:

- Contribute the Maximum: Take advantage of the full contribution limits for your chosen retirement accounts.

- Invest Wisely: Diversify your investments across different asset classes to mitigate risk and maximize returns.

- Stay Informed: Regularly monitor your investments and make adjustments as needed to keep your portfolio aligned with your goals.

- Seek Professional Advice: Consider consulting with a financial advisor to create a personalized retirement plan.

Retirement is not just a destination, it’s a journey. By understanding the different retirement accounts and implementing smart saving strategies, you can pave the way for a financially secure and fulfilling future. Don’t wait, start planning today!

Closure

Thus, we hope this article has provided valuable insights into Unlocking Your Financial Future: 5 Essential Retirement Accounts Explained. We hope you find this article informative and beneficial. See you in our next article!

google.com